Using Recurrent Convolutional Neural Network (RCNN) to Predict S&P 500 Movements

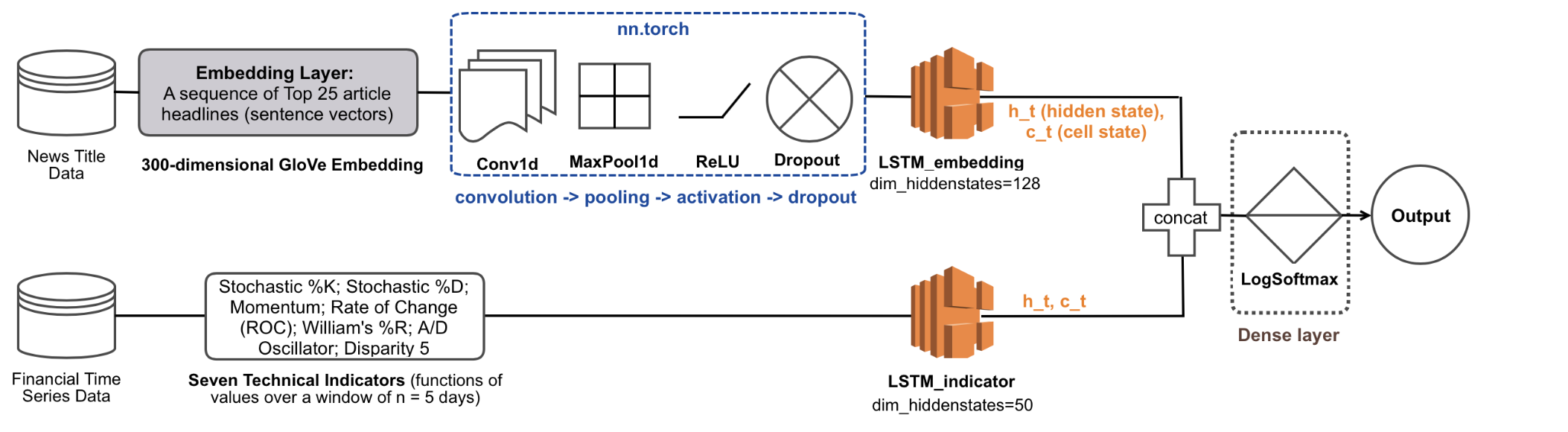

Financial news releases and time series are important data sources to predict equity market directions and movements. The existing forecasting methods mostly work with each input independently. Nowadays, with increasing computational capabilities and artificial intelligence techniques, we could combine the predicting power of both sentiment analysis and systematic signals and models. In this project, we utilize information from daily top financial news headlines and seven technical indicators: Stochastic %K, Stochastic %D, Momentum, Rate of Change, William's %R, A/D Oscillator, and Disparity 5 constructed from historical S&P 500 returns. Those hybrid inputs can extend the ability of predicting short-term equity market directional movements, achieving higher accuracies than a single source system. This project implements the architecture of a RCNN model with attention mechanism. We examine various models with or without the attention mechanism or technical indicator inputs, and the effect from different embedding methodology for the financial news headlines. Among those variations, we find that technical indicators is positively related to better performance. In addition, embedding the news headlines by averaging the vector representations for each word in the headline will outperform the model only with word embedding padded to the maximum news headline length. Furthermore, after including the attention mechanism, the model can achieve the highest accuracy among models we implemented, further coming up with a novel approach in refining the baseline model architecture.