LASSO¶

The LASSO adds a penalty to the objective

The indices for which \(\lambda_j=0\) are unpenalized.

The LASSO picture¶

Why LASSO?¶

There are several sparsity inducing penalties out there: SCAD, MCP, etc.

But we know less about the “solutions” compared to LASSO because LASSO is a convex problem.

Solvable even in very high dimensions. (“same” for SCAD, MCP, etc.)

KKT conditions give an exact description of the solution however we decide to solve it (not same for SCAD, MCP, etc), at least under uniqueness.

Solving the LASSO¶

Many algorithms out there. Many of you will end up taking EE364 (Convex Optimization) where you’ll see things like this in more detail.

We’ll consider two simple algorithms: coordinate descent, proximal gradient descent.

Everyone has their own way of talking about LASSO. These notes are just my way.

Coordinate descent¶

If the penalty \({\cal P}\) were smooth, then we could use something like Newton-Raphson as we did for fitting the GLM.

The penalty is differentiable everywhere except points where one of the \(\beta_j\)’s is 0: \(\implies\) not smooth.

However, the penalty is separable meaning

Block separability allows for a partition of \(\{1,\dots,p\}= \cup_{g \in G} g\) – group LASSO an example of this.

When the penalty is separable, the problem can be solved by successively solving low-dimensional problems.

Basic iteration¶

Each iteration \(t\) chooses a coordinate \(j\) to update. Let the current position be \(\hat{\beta}^t\) define

Coordinate descent and Gibbs sampler¶

Suppose we have a prior with independent coordinates with negative log density \({\cal P}(\beta)\).

The Gibbs sampler considers same “objective” that a coordinate descent algorithm does.

Instead of minimizing this function, it draws from a density proportional to its negative exponential.

Each iteration \(t\) chooses a coordinate \(j\) to update. Let the current position be \(\hat{\beta}^t\) draw \(\hat{\beta}^{(t+1)}_j\) from a density proportional to:

Gibbs: sample¶

Coordinate Descent: optimize¶

Coordinate descent¶

coordinate_descent = function() {

beta = rep(0, num_features)

for (i in 1:enough_iterations) {

for (j in 1:num_features) {

cur_obj = objective(X, Y, penalty, "binomial", beta, j)

beta[j] = argmax(cur_obj)

}

}

}

Gibbs sampler¶

gibbs_sampler = function() {

beta = rep(0, num_features)

for (i in 1:enough_iterations) {

for (j in 1:num_features) {

cur_post = objective(X, Y, prior, "binomial", beta, j)

beta[j] = sample_univariate(exp(cur_post))

}

}

}

Logistic regression with offset¶

Each minimization is a logistic regression with a single feature \(X_j\) and offset \(X_{-j}\hat{\beta}^{(t)}_{-j}\).

Objective with offset vector \(Z\)

Stationarity conditions

Generally speaking offset \(Z\) shifts introduces affine predictor \(\beta \mapsto X\beta + Z\).

Example with offset¶

X_sim = matrix(rnorm(200), 100, 2)

Z_sim = rnorm(100)

Y_sim = rbinom(100, 1, 0.5)

M = glm(Y_sim ~ X_sim - 1, offset=Z_sim, family=binomial);

affine_pred = X_sim %*% coef(M) + Z_sim

pi_hat = exp(affine_pred) / (1 + exp(affine_pred))

t(X_sim) %*% (Y_sim - pi_hat)

| 3.587408e-15 |

| -7.105427e-15 |

At iteration \(t\), for each \(j\), if

then

Easy to check whether a coefficient should stay or be assigned to 0…

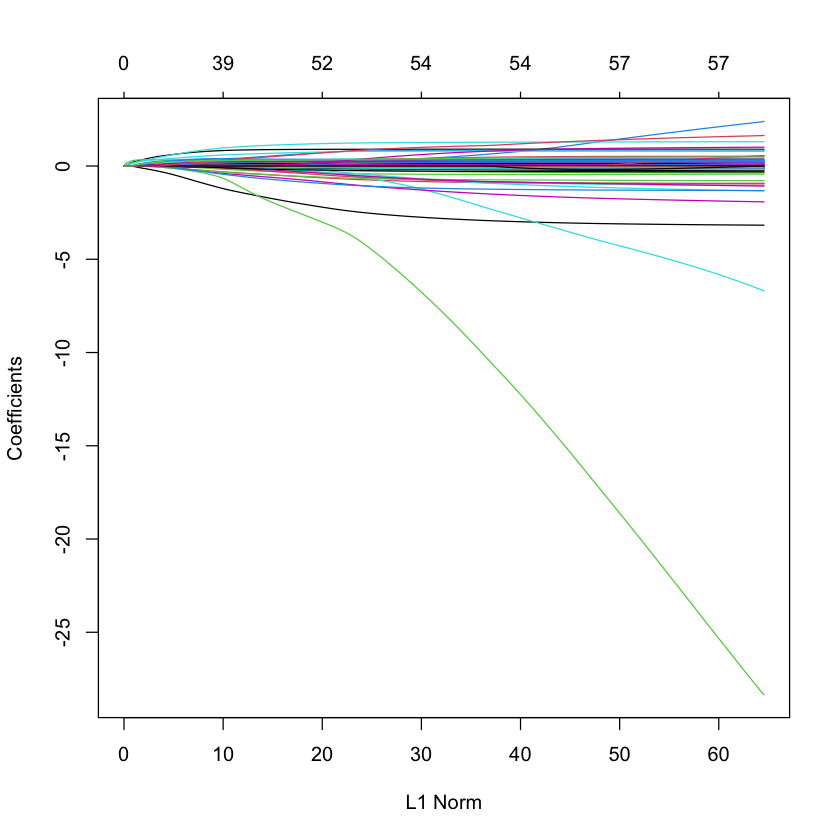

LASSO solution path for SPAM data¶

library(glmnet)

library(ElemStatLearn)

data(spam)

X_spam = scale(model.matrix(glm(spam ~ .,

family=binomial,

data=spam))[,-1]) # drop intercept

Y_spam = spam$spam == 'spam'

G_spam = glmnet(X_spam, Y_spam, family='binomial')

plot(G_spam)

Loading required package: Matrix

Loaded glmnet 4.0-2

Warning message:

“glm.fit: fitted probabilities numerically 0 or 1 occurred”

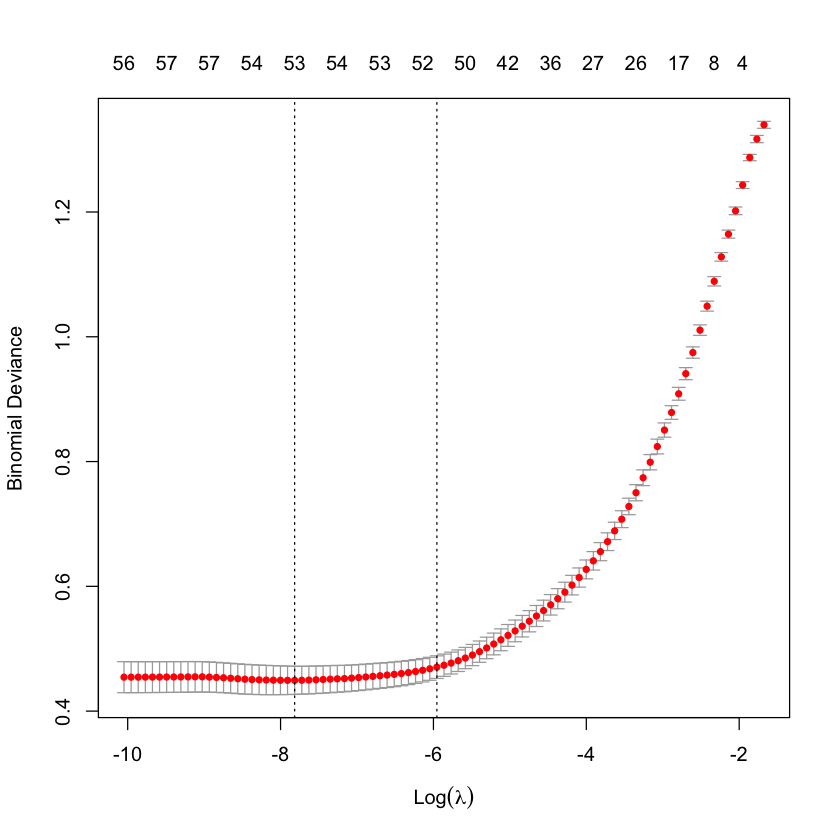

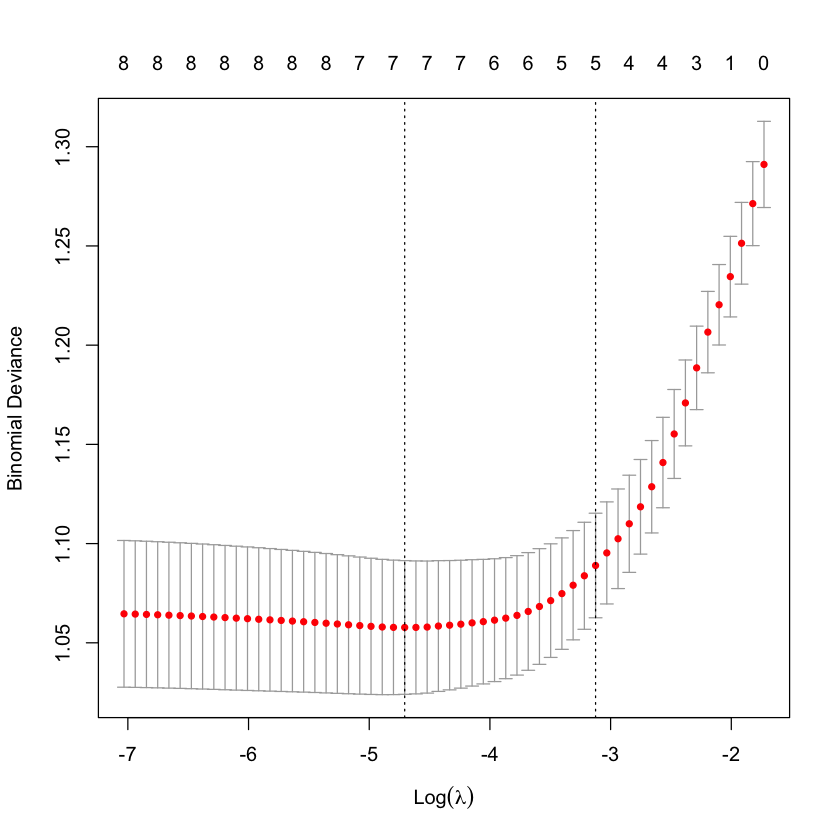

Cross-validation to choose \(\lambda\)¶

cvG_spam = cv.glmnet(X_spam, Y_spam, family='binomial')

plot(cvG_spam)

Re-solve at \(\lambda_{\min}\)¶

beta_CV_spam = coef(G_spam,

s=cvG_spam$lambda.min,

exact=TRUE,

x=X_spam,

y=Y_spam)

sum(beta_CV_spam[-1] != 0) # not very sparse in this case...

Predictions at new X¶

newX = X_spam[1:30,]

newY_hat = predict(G_spam,

newX,

s=cvG_spam$lambda.min,

type="response",

exact=TRUE,

x=X_spam,

y=Y_spam)

newY_hat[1:5]

- 0.573368457876324

- 0.979598740492402

- 0.999971117964625

- 0.747691413387677

- 0.747601439683215

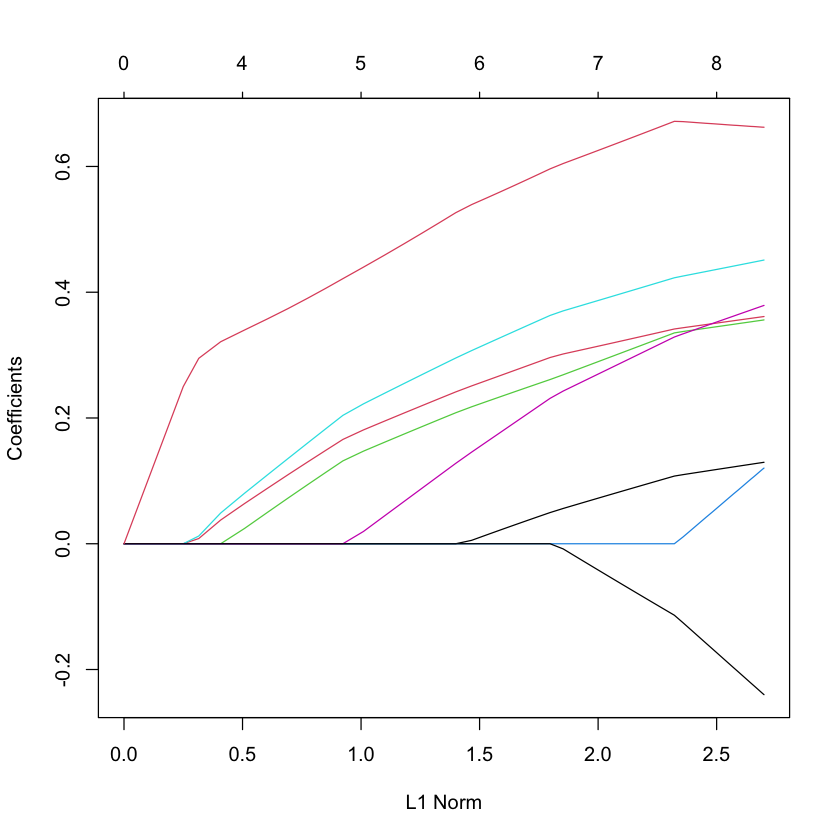

LASSO solution path for South African heart data¶

data(SAheart)

X_heart = scale(model.matrix(glm(chd ~ ., family=binomial, data=SAheart))[,-1]) # drop intercept

Y_heart = SAheart$chd

G_heart = glmnet(X_heart, Y_heart, family='binomial')

plot(G_heart)

Cross-validation to choose \(\lambda\)¶

cvG_heart = cv.glmnet(X_heart, Y_heart, family='binomial')

plot(cvG_heart)

Re-solve at \(\lambda_{1SE}\)¶

beta_1se_heart = coef(G_heart,

s=cvG_heart$lambda.1se,

exact=TRUE,

x=X_heart,

y=Y_heart)

sum(beta_1se_heart[-1] != 0) # eliminates a few

Proximal gradient descent¶

Updates all coordinates each step.

This method takes advantage of the fact that

is soft-thresholding, most importantly it is fast

Solution is

Basic update¶

Given current state \(\hat{\beta}^{(t)}\) define

The next iterate is defined as

Comments¶

Quadratic approximation similar to Newton-Raphson.

If \(L\) is chosen so that \(L \cdot I \geq \nabla^2 \ell(\beta)\) for all \(\beta\) then this is an example of Majorization-Minimization (MM) method.

Stepsize \(L\) only needs to be chosen to be a descent – backtracking typically used.

There are several accelerated proximal gradient descent algorithms out there, some local to us: NESTA, TFOCS.

Proximal algorithm is key ingredient to all of these methods.

Majorization-Minimization¶

Suppose we want to solve

We assume we have a function \(M(\beta;\beta')\) such that

Set

Then, \(f(\hat{\beta}^{(t+1)}) \leq f(\hat{\beta}^{(t)})\). Yields a descent method!

Gradient descent and Langevin sampler¶

Just as coordinate descent “looks” like Gibbs sampling. There is an analogous MCMC sampler (at least for smooth penalties…)

Langevin sampling

with \(\xi^{(t)} \sim N(0,I)\).

Reference: e.g. Dalalyan

Proximal map¶

The map

is called the proximal operator of \({\cal P}\).

Proximal gradient descent methods rely on \({\cal P}\) being fast.

Each step above evaluates the proximal map of \(L^{-1} \cdot {\cal P}\).

Reference: Parikh and Boyd

Solving the LASSO¶

LASSO in bound form¶

Original LASSO:

subject to \({\cal P}(\beta) \leq C\).

Proximal gradient descent replaces soft-thresholding with map

Solving LASSO in this form will repeatedly project

onto the convex set \(\left\{\beta: \|\beta\|_1 \leq C \right\}.\)

KKT conditions¶

How will we know we have solved

KKT conditions read

where

The set \(\partial {\cal P}(\beta)\) is called the subdifferential of \({\cal P}\) at \(\beta\).

If \({\cal P}\) is differentiable at \(\beta\), then the subdifferential is the derivative.

Can also deduce stationarity conditions from proximal gradient algorithm.

Stationarity from proximal gradient¶

If \(\hat{\beta}\) is a statitionary point of proximal gradient with step size \(L^{-1}\), then

If \(\hat{\beta}_i=0\) then

If \(\hat{\beta}_i \neq 0\) then

Very briefly, what is the subdifferential for our \({\cal P}\)?

Note that

For penalties of the form

the subdifferential is

with \(N_u(K)\) the set of normal directions at \(u \in K\).

Also characterized as

Normal cones of a cube¶

Suppose \(\hat{\beta}_{-E}=0, \min_{j \in E}|\hat{\beta}_j|>0\) and \(\text{sign}(\hat{\beta}_E)=s_E\).

Then,

In other words: active signs are fixed, inactive score is not too big.

X = matrix(rnorm(300), 100, 3)

beta = rep(0, 3)

beta[1:2] = 3

Y = X %*% beta + rnorm(100)

G = glmnet(X, Y, standardize=FALSE, intercept=FALSE)

lam = G$lam[10]

lam

beta_hat = coef(G, s=lam, exact=TRUE, x=X, y=Y)[2:4]

beta_hat

- 1.75879739460179

- 1.60004492874385

- 0

score = (t(X) %*% (X %*% beta_hat - Y) / 100)

score

lam

| -1.44969577 |

| -1.44969589 |

| 0.01360631 |

c(beta_hat[1:2], score[3])

- 1.75879739460179

- 1.60004492874385

- 0.0136063095635466

Let’s perturb \(Y\) a little and see what happens.

Y_star = Y + 0.1 * rnorm(100)

G_star = glmnet(X, Y_star, intercept=FALSE, standardize=FALSE)

beta_star = coef(G_star, s=lam, exact=TRUE, x=X, y=Y_star)[2:4]

beta_star

- 1.75907492754101

- 1.60473445347705

- 0

score_star = t(X) %*% (X %*% beta_star - Y_star) / 100

score_star

| -1.44969498 |

| -1.44969589 |

| 0.01240643 |

c(beta_star[1:2], score_star[3])

c(beta_hat[1:2], score[3])

- 1.75907492754101

- 1.60473445347705

- 0.0124064281382372

- 1.75879739460179

- 1.60004492874385

- 0.0136063095635466

KKT conditions: deeper dive¶

Restricted problem¶

Suppose variables \(E\) are selected with signs \(s_E\).

KKT equations yield

Having fixed \(E\) we can define restricted objective

First equation reads

with constraint \(\text{sign}(\hat{\beta}_E) = s_E\).

Gaussian case¶

Let’s take one Newton-Raphson step from \(\hat{\beta}_E\):

or

In the Gaussian case this reads $\( \text{sign}((X_E'X_E)^{-1}(X_E'Y - \lambda_E s_E)) = s_E. \)$

Allowing some \(\lambda_i\)’s to be zero changes things a little – only have conditions for \(\lambda_i > 0\).

Inactive block¶

Let’s look at our other set of KKT equations.

We know that

For any fixed \(E\), \(\nabla \ell(\bar{\beta}_E, 0)_{-E}\) will by asymptotically Gaussian under standard conditions. It will have mean 0 if the model \(E\) is correctly specified.

The vector

will behave as a fixed vector (with signs fixed).

Gaussian case¶

Model selection consistency¶

Now suppose that model is correct with parameter \(\beta^*\) such that \(\beta^*_{-A}=0\).

When will the LASSO recover \(A\) with correct signs \(\text{sign}(\beta^*_A)\)? (For simplicity let’s now set all \(\lambda_i\)’s equal).

References (among others): Zhao and Yu, Candes and Plan

Our look at the active block of the KKT conditions says that if we solve the restricted MLE on \(A\) and we shrink we must still have the same signs.

Up to small remainder this event is

with \(s^*_A=\text{sign}(\beta^*_A)\).

If \(\beta_A^*\) are far away enough from 0 (beta-min condition) then subtracting the second term will not change signs of \(\bar{\beta}_A\).

Let’s look at the inactive block. We saw that if the active set is going to be \(A\) and signs \(s_A^*\) then

For this to happen, essentially we need the irrepresentable condition (Zhao and Yu)

How large should \(\lambda\) be?¶

The irrepresentable condition suggests \(\lambda\) should be such that $\( \|\nabla \ell(\bar{\beta}_A, 0)_{-A}/\lambda\|_{\infty} < 1. \)$

A typical choice

Such choice often guarantees LASSO is consistent. (Large literature on this, c.f. Negabhan et al.)