Penalized regression¶

The objective function for a GLM (as a minimization) can be written as

With some abuse of notation

and \(\Lambda\) is the log MGF of \(Y\)’s as a function of the natural parameter.

Penalized regression¶

Objective:

Three examples we’ve seen:

Gaussian \(\Lambda(\alpha) = \alpha^2/2\) (or scale objective \(\sigma^2\));

Logistic \(\Lambda(\alpha) = \log(1 + e^{\alpha})\).

Poisson log-linear \(\Lambda(\alpha) = e^{\alpha}\).

Ridge regression¶

Ridge regression adds a quadratic pnalty

Estimator

Features are usually centered and scaled so coefficients are unitless.

“Bayesian” interpretation¶

If we were to put a \(N(0, \lambda^{-1} I)\) prior on \(\beta\) its log posterior would be (up to normalizing constant depending only on \((X,Y)\))

Ridge estimator yields MAP (Maximum A Posteriori) estimator (i.e. the posterior mode).

Easy to add weights¶

unpenalized variables have \(\lambda_j=0\).

General quadratics also fine¶

Corresponds to \(N(0,Q^{-1})\) prior.

Overall objective¶

Solving for the ridge estimator¶

From unpenalized case we know 2nd Taylor approximation of likelihood.

Differentiating the penalty:

Newton-Raphson / Fisher scoring¶

For canonical models

General form

Not the only way to solve this problem…

Why do we regularize?¶

Consider Gaussian case with \(Q=\lambda I\)

Writing \(X=UDV'\) we see

Bias¶

Writing \(\beta=\sum_j \alpha_j V_j\):

Variance¶

RHS is trace of \(\text{Var}((X'X)^{-1}(X'Y))\).

Ridge always has smaller variance.

MSE¶

Assuming \(\beta \neq 0\)

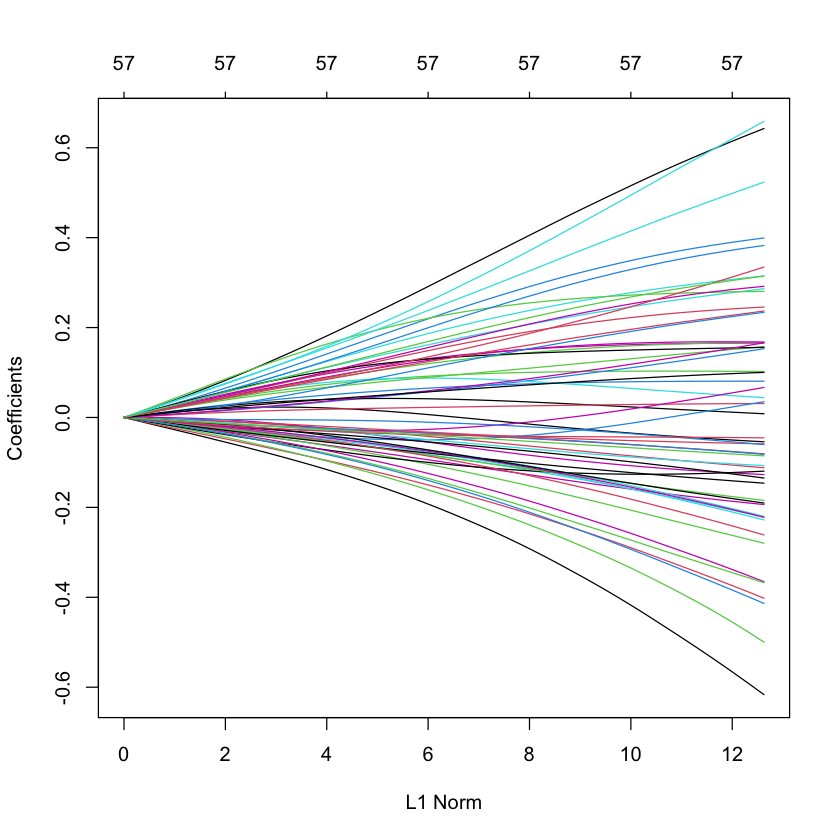

Ridge solution path for SPAM data¶

library(glmnet)

library(ElemStatLearn)

data(spam)

X_spam = scale(model.matrix(glm(spam ~ .,

family=binomial,

data=spam))[,-1]) # drop intercept

Y_spam = spam$spam == 'spam'

G_spam = glmnet(X_spam,

Y_spam,

alpha=0, # this makes it ridge

family='binomial')

plot(G_spam)

Loading required package: Matrix

Loaded glmnet 4.0-2

Warning message:

“glm.fit: fitted probabilities numerically 0 or 1 occurred”

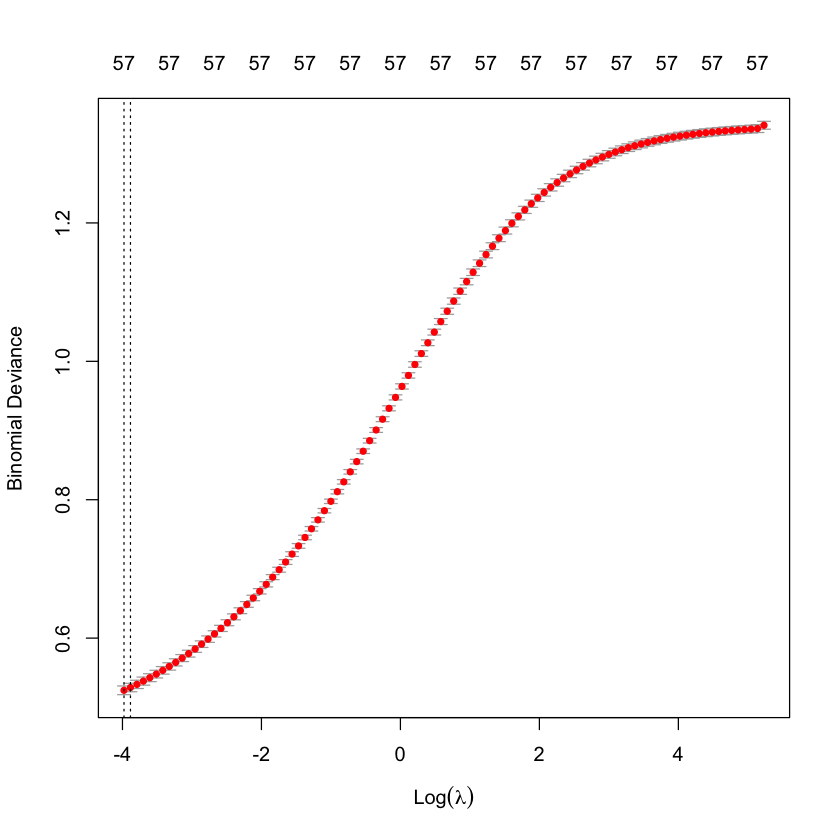

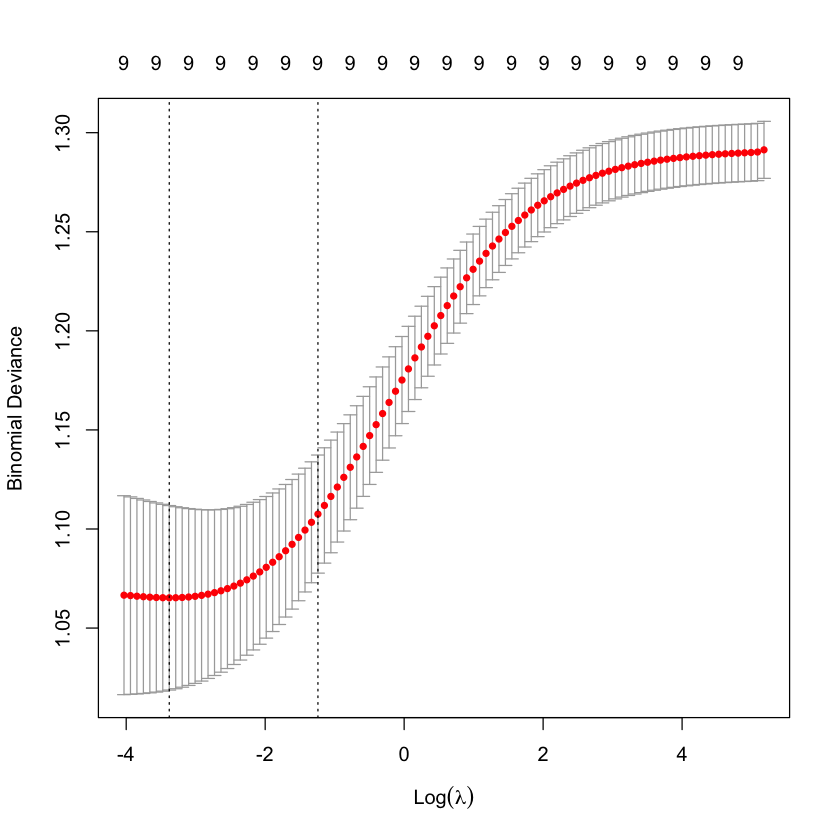

Cross-validation to choose \(\lambda\)¶

cvG_spam = cv.glmnet(X_spam,

Y_spam,

alpha=0,

family='binomial')

plot(cvG_spam)

Re-solve at \(\lambda_{\min}\)¶

beta_CV_spam = coef(G_spam,

s=cvG_spam$lambda.min,

exact=TRUE,

x=X_spam,

y=Y_spam,

alpha=0)

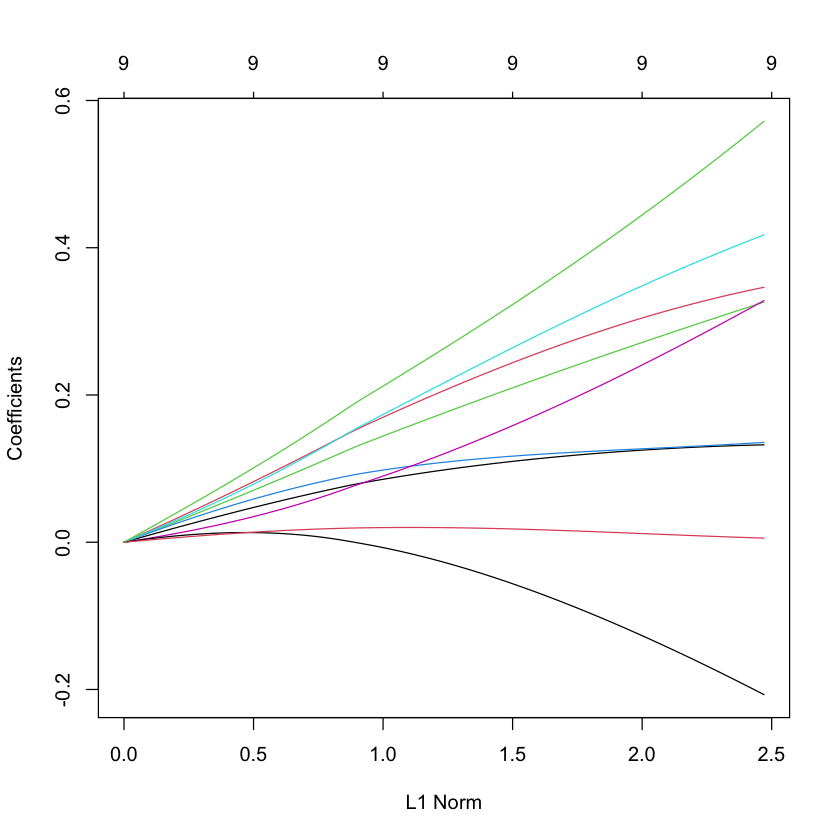

Ridge solution path for South African heart data¶

data(SAheart)

X_heart = scale(model.matrix(glm(chd ~ ., family=binomial, data=SAheart))[,-1]) # drop intercept

Y_heart = SAheart$chd

G_heart = glmnet(X_heart,

Y_heart,

alpha=0,

family='binomial')

plot(G_heart)

Cross-validation to choose \(\lambda\)¶

cvG_heart = cv.glmnet(X_heart,

Y_heart,

alpha=0,

family='binomial')

plot(cvG_heart)

Re-solve at \(\lambda_{1SE}\)¶

beta_1se_heart = coef(G_heart,

s=cvG_heart$lambda.1se,

exact=TRUE,

alpha=0,

x=X_heart,

y=Y_heart)