Structured#

Download#

Fixing \(\Sigma\), solve for \(\gamma\)

Solving for optimal \(\Sigma\) seems messy, could just plug in unbiased estimate

TRUE

Reduced rank regression: rank 1#

The null \(H_0:B(I - \frac{1}{q}11^T)=0\) says that \(B=\gamma 1^T\), i.e. the \(q\) different regressions share parameters \(\gamma\).

This imposes some structure on \(B\). In this case \(B\) is rank 1 (and we have fixed its row space).

A natural generalization is to remove constraint that row space is \(1\):

Model#

If we knew \(V\) $\( YV \sim N(XUV^TV, I \otimes V^T\Sigma V) = N((V^TV) \cdot XU, V^T\Sigma V \cdot I) \)$

Design matrix has one column!

Regression with a univariate response.

This model says that \(Y|X\)’s variation is driven by \(XU\) though in possibly different directions determined by columns of \(V\).

Fitting this model for given \(\Sigma\) we need to solve

Differentiate wrt \(V\) for fixed \(U\) yields score equation

Substituting \(\widehat{V}\) yields the problem

Many minimizers here, let’s pick one…

Let \(\widehat{W}\) be the leading unit eigenvector of

and set \(\widehat{U}=(X^TX)^{-1/2}\widehat{W}\), noting that \((X\widehat{U})^TX\widehat{U} = 1\).

Can also plugin \(\widehat{\Sigma}=Y^T(I-P_F)Y / (n-p)\).

Plugging into expression for \(V\) yields

and

with \(\widehat{B}=(X^TX)^{-1}X^TY\) the unrestricted MLE.

An equivalent expression

where \(\widehat{Z}\) is the leading unit eigenvector of

Relation to CCA#

Common to choose \(\widehat{U}\) so that \(X\widehat{U}\) has standard deviation 1. Similarly, \(Y\widehat{V}\) is another \(n\)-vector that can be scaled to have standard deviation 1.

In fact, any pair \(U, V\) determine two such \(n\)-vectors. We might look at

The maximizing \((U,V)\) are the \((\widehat{U}, \widehat{V})\) we derived above up to a scaling by the maximized correlation.

We will revisit this when we talk about canonical correlations (Chapter 10 of MKB)

General case: rank \(k\)#

Let us now take \(U \in \mathbb{R}^{p \times k}, V \in \mathbb{R}^{q \times k}\) with \(k < \text{min}(n,p)\).

Model has \(O(k(q+p))\) parameters, can be much smaller than \(qp\) if, say, \(p\) is large and \(q\) is moderate.

Given \(U\), the optimal \(V\) is the same

To find \(\widehat{U}\) we must solve $\( \text{minimize}_{U \in \mathbb{R}^{p \times k}} -\frac{1}{2} \text{Tr}\left(\Sigma^{-1}Y^TXU((XU)^TXU)^{-1}(XU)^TY\right) \)$

Note that objective is unchanged if we replace \(U\) with \(UA\) for non-singular \(A_{k \times k}\).

We can choose \(U\) such that \(U^T(X^TX)U=I_{k \times k}\)…

A very useful fact#

Suppose \(\mathbb{R}^{m \times m} \ni M=M^T \geq 0\). Consider

Matrix \(M\) has an eigendecomposition:

If \(\lambda(M)\) has no ties at \(\lambda_k(M)\), then

With ties in \(\lambda_i(M)\) eigendecomposition is not unique. Minimizers still formed by taking \(k\) eigenvectors corresponding to top \(k\) eigenvalues.

Proof:#

Von Neumann trace inequality for (symmetric) matrices \(A,B\)

When \(B=UU^T\) is a rank \(k\) projection and \(A \geq 0\)

Our proposal achieves this value…

General version of inequality with \(\sigma_i(A)\) the singular values:

Finishing reduced rank#

Let \(\widehat{W}\) be such that \(\widehat{W}\widehat{W}^T\) is the (orthogonal) projection onto the rank top \(k\) eigenvectors of \((X^TX)^{-1/2}X^TY \Sigma^{-1} Y^TX (X^TX)^{-1/2}\) and set \(\widehat{U}=(X^TX)^{-1/2}\widehat{W}\).

Answer is identical to rank 1 case, though the matrices \(\widehat{Z}, \widehat{W}\) have more than one column now.

Common to plug in \(\widehat{\Sigma}=Y^T(I-1/n 11^T)Y/(n-1)\), though answer is the same with \(\widehat{\Sigma}=Y^T(I-P_F)Y/(n-p)\) (Exercise 3.22 in ESL).

Starting point#

This follows

rrrvignette here

#| echo: true

library(rrr)

data(tobacco)

str(tobacco)

Attaching package: ‘rrr’

The following object is masked from ‘package:stats’:

residuals

'data.frame': 25 obs. of 9 variables:

$ Y1.BurnRate : num 1.55 1.63 1.66 1.52 1.7 1.68 1.78 1.57 1.6 1.52 ...

$ Y2.PercentSugar : num 20.1 12.6 18.6 18.6 14 ...

$ Y3.PercentNicotine : num 1.38 2.64 1.56 2.22 2.85 1.24 2.86 2.18 1.65 3.28 ...

$ X1.PercentNitrogen : num 2.02 2.62 2.08 2.2 2.38 2.03 2.87 1.88 1.93 2.57 ...

$ X2.PercentChlorine : num 2.9 2.78 2.68 3.17 2.52 2.56 2.67 2.58 2.26 1.74 ...

$ X3.PercentPotassium : num 2.17 1.72 2.4 2.06 2.18 2.57 2.64 2.22 2.15 1.64 ...

$ X4.PercentPhosphorus: num 0.51 0.5 0.43 0.52 0.42 0.44 0.5 0.49 0.56 0.51 ...

$ X5.PercentCalcium : num 3.47 4.57 3.52 3.69 4.01 2.79 3.92 3.58 3.57 4.38 ...

$ X6.PercentMagnesium : num 0.91 1.25 0.82 0.97 1.12 0.82 1.06 1.01 0.92 1.22 ...

Extract \(X\) and \(Y\)#

#| echo: true

library(dplyr)

tobacco <- as_tibble(tobacco)

tobacco_x <- tobacco %>%

select(starts_with("X"))

tobacco_y <- tobacco %>%

select(starts_with("Y"))

Attaching package: ‘dplyr’

The following objects are masked from ‘package:stats’:

filter, lag

The following objects are masked from ‘package:base’:

intersect, setdiff, setequal, union

#| echo: true

Y = as.matrix(tobacco_y)

X = as.matrix(tobacco_x)

lm(Y ~ X)

Call:

lm(formula = Y ~ X)

Coefficients:

Y1.BurnRate Y2.PercentSugar Y3.PercentNicotine

(Intercept) 1.41114 13.63291 -1.56482

XX1.PercentNitrogen 0.06197 -4.31867 0.55216

XX2.PercentChlorine -0.16013 1.32629 -0.27856

XX3.PercentPotassium 0.29212 1.58995 0.21759

XX4.PercentPhosphorus -0.65798 13.95265 -0.72311

XX5.PercentCalcium 0.17303 0.55259 0.32309

XX6.PercentMagnesium -0.42835 -3.50211 2.00486

#| echo: true

rrr(X, Y, type='identity', rank=2)

- $mean

A matrix: 3 × 1 of type dbl 3.4740985 13.9605303 -0.5117545 - $A

A matrix: 3 × 2 of type dbl 0.03107787 -0.4704307 -0.97005030 0.1984637 0.24090782 0.8598297 - $B

A matrix: 2 × 6 of type dbl X1.PercentNitrogen X2.PercentChlorine X3.PercentPotassium X4.PercentPhosphorus X5.PercentCalcium X6.PercentMagnesium 4.3242696 -1.35864835 -1.4808316 -13.729424 -0.4528289 3.866896 -0.4114869 0.09903401 0.3652138 2.456879 0.3060762 1.230305 - $C

A matrix: 3 × 6 of type dbl X1.PercentNitrogen X2.PercentChlorine X3.PercentPotassium X4.PercentPhosphorus X5.PercentCalcium X6.PercentMagnesium 0.3279651 -0.08881253 -0.21782885 -1.582473 -0.1580606 -0.4585985 -4.2764242 1.33761189 1.50896282 13.805833 0.5000118 -3.5069123 0.6879417 -0.24215663 -0.04272224 -1.195028 0.1540834 1.9894186 - $eigen_values

-

- 3.2820997448457

- 0.0378297755314835

- 0.0101599583310807

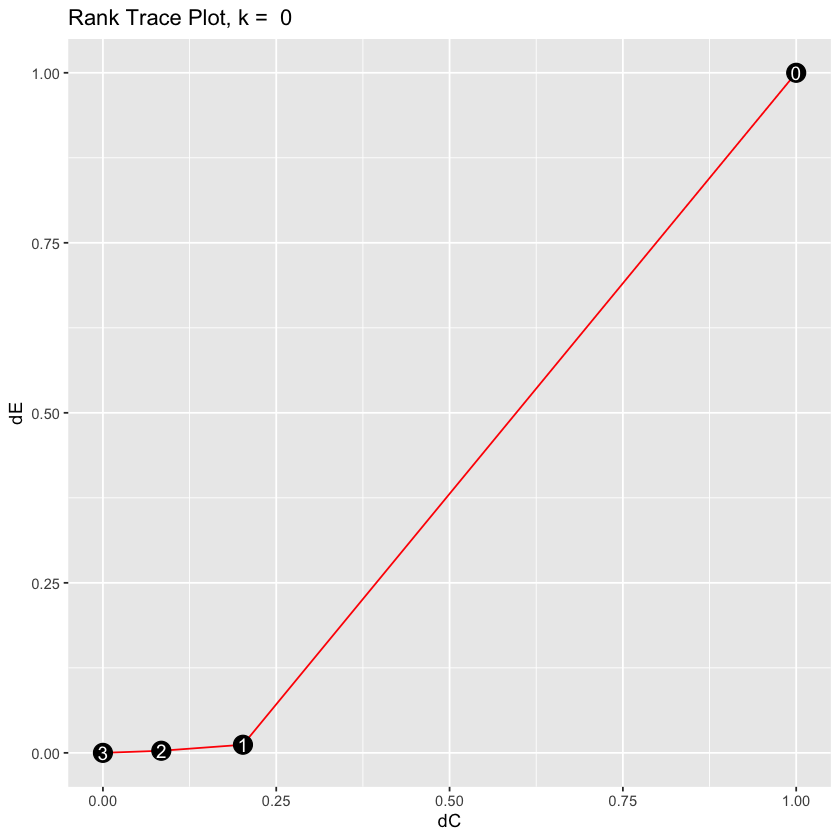

#| echo: true

rank_trace(X, Y, type='identity')

Warning message:

“`data_frame()` was deprecated in tibble 1.1.0.

ℹ Please use `tibble()` instead.

ℹ The deprecated feature was likely used in the rrr package.

Please report the issue to the authors.”

Warning message:

“`as_data_frame()` was deprecated in tibble 2.0.0.

ℹ Please use `as_tibble()` (with slightly different semantics) to convert to a tibble, or `as.data.frame()` to convert

to a data frame.

ℹ The deprecated feature was likely used in the rrr package.

Please report the issue to the authors.”

Warning message:

“The `x` argument of `as_tibble.matrix()` must have unique column names if `.name_repair` is omitted as of tibble

2.0.0.

ℹ Using compatibility `.name_repair`.

ℹ The deprecated feature was likely used in the tibble package.

Please report the issue at <https://github.com/tidyverse/tibble/issues>.”

Sparsity#

LASSO?#

Of course, there are other types of structure…

Usually \(X\) will be centered and standardized to make features comparable

Often \(\Sigma=I\) is used: decouples likelihood into \(q\) terms

Sparsity is not shared in any sense: \(q\) separate LASSO problems $\( \text{minimize}_{B[,j], 1 \leq j \leq q} \sum_{j=1}^q \left[\frac{1}{2} \|Y[,j]-XB[,j]\|^2_2 + \lambda \|B[,j]\|_1 \right] \)$

Some methods don’t require plugging in \(\Sigma\)

Group sparsity#

The blockwise group-LASSO could be used

Yields solutions that zero out entire rows of \(B\) – drops some features!

Reference: Obozinski et al.

Sometimes \(\|\cdot\|_{\infty}\) is used.

Group LASSO#

Suppose \(\{1, \dots, p\}\) is partitioned as \(\{g_1, \dots, g_k\}\) (i.e. disjoint groups).

Generically, for large values of \(\lambda\) if we solve a (convex) problem

we will see several \(\widehat{\beta}[g_j]\) = 0. Why?

In the multivariate regression case, grouping the rows of \(B\) together gives us solutions where several rows are exactly 0.

Why do we get exact zeros?#

Properties of a penalty \({\cal P}\) can be determined from its proximal map

Let’s consider one group:

Differentiating yields equation (where differentiable)

Clearly if there is a solution \(\widehat{z}(y) = c \cdot y\) and it is enough to solve

Optimal \(c\) is \(\max(1 - \lambda / \|y\|_2, 0)\):

Norm of solution \(\max(\|y\|_2 - \lambda, 0)\): soft-thresholding the norm.

What it means to solve the group LASSO#

Solving group LASSO with groups as rows of \(B\) yields \(\widehat{B}\).

Also yields subgradient

Subgradient equation (KKT) analog of critical point (first order) condition for smooth optimization problems.

In this case, it must be that

and

We see the subgradient \(\widehat{U}\) is tied to \(\widehat{B}\).

Solving the group LASSO means producing a pair \((\hat{B}, \hat{U})\).

Inverting the KKT conditions#

This pairing \((\widehat{B}, \widehat{U})\) also tells us how to construct solutions. For simplicity, we’ll assume \(n > p\) so that \(X^TX\) is non-singular and we’ll take \(\Sigma=I\)

Subgradient equation at a solution \((\widehat{B}, \widehat{U})\) can be rewritten as

In other words, the map \(X^TY \mapsto (\widehat{B}, \widehat{U})\) is (essentially) invertible.

Conditioning on \(X\), to construct a \(Y\) whose group LASSO solution is a given \((B_0, U_0)\) set

Can be used for inference via estimator augmentation, basis for results on consistency of variable selection.

Solving the problem#

Blockwise descent#

For each \(1 \leq i \leq p\) fix \(\widehat{B}[-i]\) and minimize only over \(B[i]\) $\( \text{minimize}_{B[i] \in \mathbb{R}^q} \frac{1}{2} \left\|Y - \sum_{l \neq i} X[,l] \widehat{B}[l] - X[,i] B[i]\right\|^2_F + \lambda w_i \|B[i]\|_2 \)$

Repeat step 1. over until convergence.

Proximal gradient descent#

Initialize \(\widehat{B}^{(0)}=0\), say.

For step size \(\alpha=L^{-1}\) set $\( \widehat{B}^{(k+1)} = \text{argmin}_B \frac{L}{2} \|B - (\widehat{B}^{(k)} - 1/L \nabla \ell(\widehat{B}^{(k)})) \|^2_F + \lambda \sum_{i=1}^p w_i \|B[i,]\|_2 \)$

Proximal gradient descent as an MM-algorithm#

Suppose we want to solve, for a smooth loss \(\ell\) and penalty \({\cal P}\):

Given a current value \(\hat{\beta}^{(t)}\), consider a penalized 2nd order Taylor expansion of the smooth loss:

Now suppose we pick \(L=L(\hat{\beta}^{(t)})\) such that (in the PSD ordering)

Majorizing function#

Define

Claims:#

\(G(\beta;\beta) = \ell(\beta) + {\cal P}(\beta)\)

For each \(\bar{\beta}\), \(G(\beta;\bar{\beta}) \geq \ell(\beta) \qquad \forall \beta\)

\(\implies\) the following sequence is a descent sequence:

I.e. \(\ell(\hat{\beta}^{(t+1)}) + {\cal P}(\hat{\beta}^{(t+1)}) \leq \ell(\hat{\beta}^{(t)}) + {\cal P}(\hat{\beta}^{(t)})\).

Other penalties#

Sparse group LASSO#

There are lots of penalties out there… $\( \text{minimize}_{B} \frac{1}{2} \|Y-XB\|^2_F + \lambda_1 \sum_{i} \|B[i,]\|_2 + \lambda_2 \sum_i \|B[i,]\|_1 \)$

Nuclear norm#

A convex way to get a low-rank solution

For application to regression setting Yuan et al.

Proximal map is

where \(Z=UDV^T\) and \(S_{\lambda}(D)\) is elementwise soft-thresholding at \(\lambda\) – kills terms with singular values less than \(\lambda\).

Group sparse + low rank#

One can start to combine penalties…

Multitask regression#

Multivariate regression is not only context where parameters \(B\) is a matrix.

Multitask: we observe \(q\) different datasets \((X_j, Y_j)\) and loss is $\( \ell(B) = \sum_{j=1}^q \|Y_j - X_j B[,j]\|^2_2 \)$

Parameter decomposition

Expresses \(B\) as main effects plus interactions (i.e. group specific effects).

Data shared LASSO $\( \text{minimize}_{\beta, \Delta} \sum_{j=1}^q \frac{1}{2} \|Y_j - X_j (\beta + \Delta[,j])\|^2_2 + \lambda \|\beta\|_1 + \lambda' \sum_{i=1}^p \|\Delta[i,]\|_1 \)$

Can be fit with

glmnet– a LASSO with expanded design matrix.Such a penalty can be used for multivariate regression as well: models a common regression function plus sparse interactions.

Other models: glinternet, heirnet, pliable LASSO, UniLASSO